Imagine Never Waiting for a Wire Transfer Again

You send money from your U.S. bank to a friend abroad. The bank says, “It’ll take 3–5 business days.” Three days pass. Still pending. Frustrating, right?

Now imagine sending that same money, and it arrives in minutes: no middlemen, no hidden fees, no weird delays.

That’s not a dream. That’s blockchain, and it’s already reshaping how banks work behind the scenes.

So… What Exactly Is Blockchain?

Let’s strip away the tech-speak.

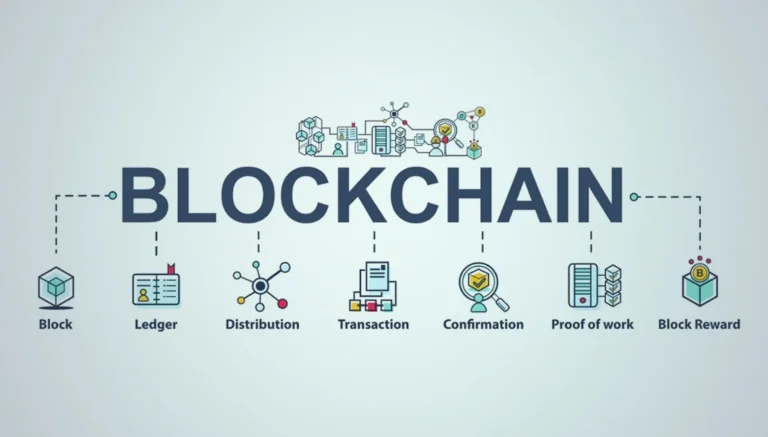

At its core, blockchain is a digital record-keeping system. Think of it like a giant spreadsheet that lives on many computers at once. Every time someone adds a new transaction (like sending money), it’s recorded across all those computers. It’s secure, transparent, and very hard to tamper with.

Now, here’s the magic: nobody owns this spreadsheet. It’s shared, verified by multiple users, and can’t be changed without everyone knowing. That’s why people trust it.

Why Should You Care?

The U.S. banking system is built on layers of outdated tech, middlemen, and slow processes. Blockchain is cutting through all that, making things faster, safer, and cheaper.

And the shift is already happening. From JPMorgan Chase to Bank of America, major players are experimenting with blockchain to:

Move money across borders

Verify identities securely

Prevent fraud and errors

Automate contracts and loan approvals

If you’ve ever been frustrated by slow banking processes, sneaky fees, or the sheer complexity of things like loans or wire transfers, you’ll want to keep reading.

1. Faster, Cheaper Payments (Especially International)

Let’s start with a common pain: sending money abroad.

Right now, U.S. banks rely on systems like SWIFT, which involve middlemen (called correspondent banks). Each stop takes time and adds a fee. That’s why international transfers often feel like a money maze.

Blockchain changes that.

Example:

JPMorgan’s JPM Coin allows instant settlement between institutional clients using blockchain. Other banks are using Ripple, a blockchain network designed for fast international payments.

How it helps you:

Transfers can happen in seconds or minutes

Lower fees—no hidden charges from intermediaries

Less room for delays or errors

2. Fighting Fraud and Improving Security

Identity theft. Account hacks. Credit card fraud. If these sound familiar, you’re not alone.

U.S. banks lose billions every year to fraud. One of blockchain’s biggest strengths is security. It’s built to resist tampering.

Every transaction is locked with a digital signature. Once it’s on the chain, it can’t be changed. Plus, the decentralized nature of blockchain means there’s no single point of failure.

Example:

Bank of America has filed patents for blockchain-based fraud detection. Others are exploring blockchain to store customer identity data securely, making it harder for criminals to impersonate people.

Why this matters to you:

Less chance of someone opening credit in your name

Fewer phishing or spoofing attacks

More trust in digital banking platforms

3. Smart Contracts: No More “Lost Paperwork”

Ever signed a loan agreement, then waited days for someone to “review and approve” it?

Now, imagine a digital contract that executes itself when the terms are met. That’s a smart contract, and blockchain powers it.

These digital agreements sit on the blockchain and automatically run when both parties meet the conditions. No human delays. No “oops, we missed your file.”

Example:

Startups and banks alike are testing smart contracts for mortgage approvals, business loans, and insurance claims.

Benefits for customers:

Quicker loan decisions

Less paperwork and bureaucracy

Reduced chance of human error

4. Better KYC (Know Your Customer)

Every time you open a new account, apply for a mortgage, or set up a credit card, you go through KYC—a fancy name for “proving you are who you say you are.”

Currently, every bank does this separately. Blockchain can store a verified, secure identity profile that banks can access (with your permission). You don’t need to send your driver’s license five times to five institutions.

Real-world impact:

Easier onboarding with banks or apps

Faster loan or credit applications

Less chance of your identity being stolen

5. Tokenized Assets and Digital Currencies

Here’s where it gets interesting.

Banks are exploring tokenization, which means turning physical or traditional assets into digital versions on a blockchain.

Think of owning a fraction of real estate, art, or even stocks as tokens you can trade instantly.

At the same time, the U.S. Federal Reserve is considering a CBDC (Central Bank Digital Currency)—a government-backed digital dollar.

What this means:

Faster, traceable transactions

Easier access to investments

Potentially more financial inclusion

6. Cutting Costs Behind the Scenes

You may never see this directly, but banks spend billions of dollars every year reconciling data, checking that what Bank A says matches what Bank B says.

With blockchain, everyone sees the same record in real time. This means:

Less back-office work

Fewer disputes

Lower operating costs (which may eventually benefit you)

Santander estimated that blockchain could save the global banking industry $15–20 billion annually in infrastructure costs.

But It’s Not All Perfect Yet…

Before you toss your debit card in excitement, let’s be honest: blockchain isn’t a silver bullet.

Here are a few hurdles:

Scalability: Blockchains can be slower than traditional databases when overloaded.

Regulation: U.S. laws are still catching up with the technology.

Energy use: Some older blockchain models consume a lot of power, though this is improving.

Still, banks and governments are working on solutions, and the momentum is undeniable.

The Human Side of Blockchain Banking

Let’s take a step back from the tech.

Imagine you’re a small business owner in Texas. You just sold a batch of handmade goods to a buyer in Germany. Instead of juggling PayPal, bank wires, and a week of waiting, you send payment on a blockchain-powered app. It arrives in minutes, and you both save money.

Or maybe you’re a student in Chicago trying to send money home to family in Mexico. Blockchain can make that process faster, cheaper, and less stressful.

These stories are real, and they’re growing. At its heart, blockchain in banking is about removing friction. It’s about giving people more control, speed, and security in how they manage money.

So, What Does the Future Look Like?

Banks in the U.S. won’t flip a switch overnight, but we’re already seeing big steps.

Here’s what to expect in the next few years:

More banks are partnering with blockchain startups

Easier access to crypto services through traditional banks

Digitized IDs for smoother onboarding

Fully digital mortgage and loan processes

Real-time international payments without third-party fees

Key takeaway: Blockchain isn’t replacing banks. It’s transforming how they work, often in ways that benefit everyday users.

Keep an Eye on Your Bank

Your bank may not say the word “blockchain” in its app. But the changes are happening in the background—faster payments, smarter systems, better protection.

If you’re someone who:

Hates slow transfers

Worries about fraud

Wants easier access to financial tools

…then blockchain-powered banking is something to watch. It’s not just for crypto enthusiasts or tech nerds anymore. It’s becoming part of how banks serve real people like you and me.

And honestly? About time.

Quick Recap: Blockchain in Banking – What’s Changing?

| Use Case | How It Helps You |

|---|---|

| International Payments | Faster, cheaper, more reliable transfers |

| Fraud Prevention | Safer data, fewer hacks |

| Smart Contracts | Faster loan processing, less paperwork |

| KYC | Easier identity verification |

| Digital Assets | New ways to invest and access value |

| Back-End Savings | Lower costs that may lead to better services |